Credit Management

Credit Report

What is a credit report?

A credit report contains information about your credit, bill repayment history and

the status of your credit accounts. This information includes how often you make your

payments on time, how much credit you have, how much credit you have available, how

much credit you are using and whether a debt or bill collector is collecting on money

you owe. Make sure you review your credit report to ensure that the information is

accurate. If there are any discrepancies contact the credit reporting agency that

provided the report containing the error. Check your credit report for errors and

discrepancies at least once a year at AnnualCreditReport.com.

Who collects and reports credit information?

There are three major credit bureaus: Equifax, Experian and TransUnion that gather and maintain information about you that is included in your credit report.

The credit bureaus provide this information to companies or persons that request it,

in the form of a credit report.

Where do credit bureaus get their information?

Credit bureaus get information from your creditors, such as banks, credit card issuers

or auto finance companies. They also gather information about you from public records.

Information in one credit bureau's report may be different from the information in

another credit bureau's report because each credit bureau gets its information from

different sources.

How long does information remain on your credit report?

Positive information remains on your credit report indefinitely. Negative information

remains on your credit report between seven and 10 years. Credit inquiries remain

on your credit report for up to two years. When you apply for credit, you authorize

lenders to ask or "inquire" for a copy of your credit report from a credit bureau.

Who is allowed to see my credit report?

Credit bureaus can provide credit reports only to: lenders from whom you are seeking

credit, lenders that have granted you credit, phone and utility companies that may

provide services to you, your employer (only if you agree), insurance companies, government

agencies and anyone else with a legitimate business need for the information (e.g.

landlords or banks). If you're concerned about unauthorized access, you can place

a credit freeze or fraud alert on your report to restrict access.

Where to obtain a free credit report?

- www.annualcreditreport.com

- www.creditkarma.com

- You can request a free credit file disclosure, commonly called a credit report, once

every 12 months from each of the nationwide consumer credit reporting companies: Equifax,

Experian and TransUnion.

Disputing Errors on Credit Reports - Tell the credit reporting company, in writing, what information you think is inaccurate. Sample Dispute Letter - Consumer Credit Reporting Companies

- Equifax

O. Box 740241

Atlanta, GA 30374-0241

1-800-685-1111 - Experian

O. Box 2104

Allen, TX 75013-0949

1-888-EXPERIAN (397-3742) - Trans Union

O. Box 1000

Chester, PA 19022

1-800-916-8800

- Equifax

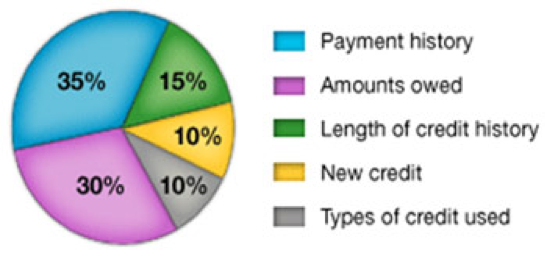

How a FICO Credit Score Breaks Down: