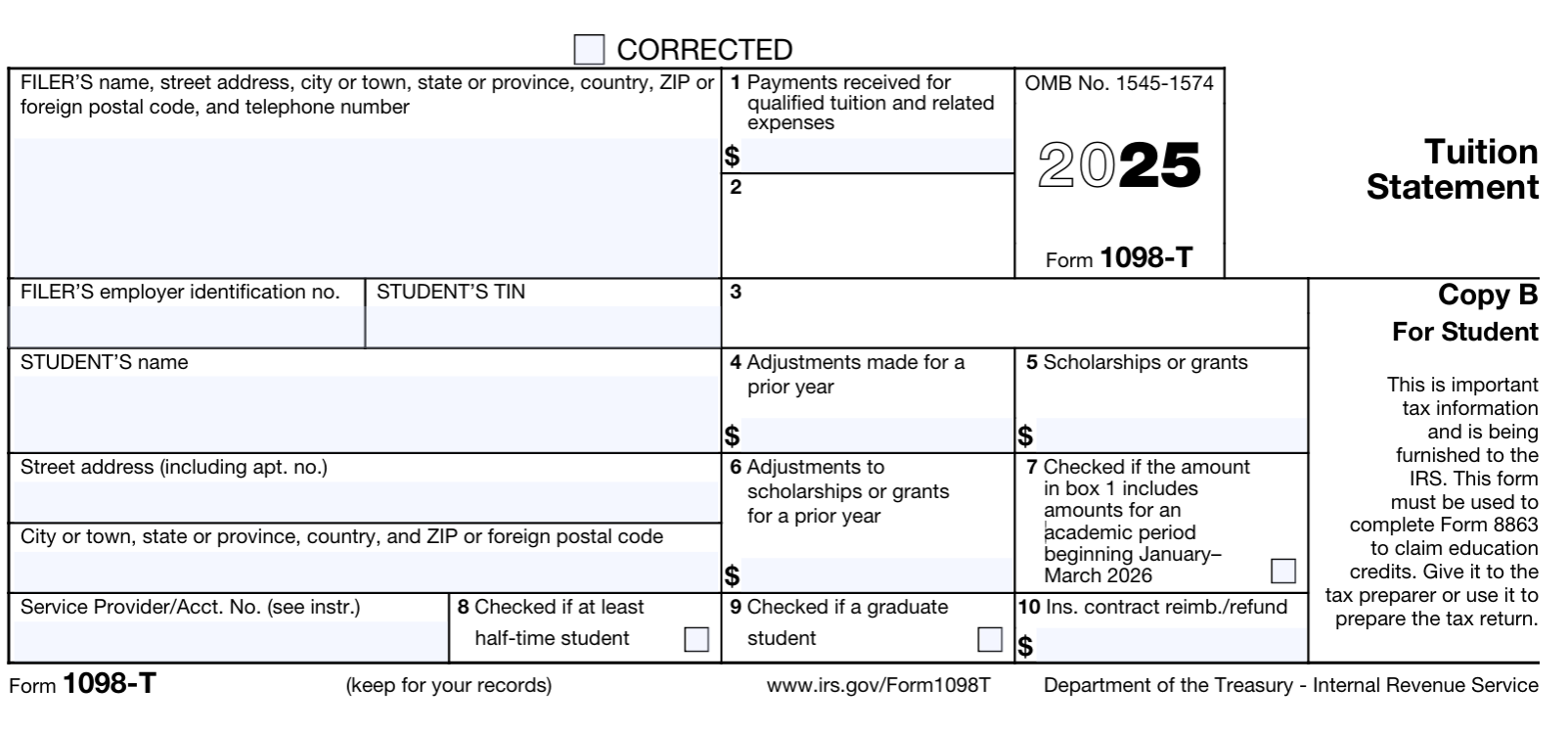

Box 1- The total payments from any source received by an eligible educational institution

in 2018 for qualified tuition and related expenses less any reimbursements or refunds

made during 2018 that relate to payments received during 2018. Please note the amount

in Box 1 will NOT equal to or sum to the charges paid for calendar year 2018 because all charges are

not considered qualified tuition and related expenses as defined by the Internal Revenue

Service. Health fees and counseling fees are not qualified; therefore, the full amount

of the Program and Services Fee paid will not be reported.

Box 2- Blank

Box 3-Shows whether the University of Tennessee changed its method of reporting for 2018.

This box will be checked.

Box 4- The amount of any adjustments made for a prior year for qualified tuition and related

expenses that were reported on a prior year Form 1098-T. This amount may reduce any

allowable education credit you may claim for the prior year. See Form 8863 or the

IRS Pub 970 for more information.

Box 5- This box includes the total of all scholarships, grants, Internal NPE’s and fee waivers

administered and processed by the University.

Box 6- This will be the amount of any adjustments made for prior year scholarships, Internal

NPE’s grants, and fee waivers that were reported on a prior year Form 1098-T. This

amount may reduce any allowable education credit you may claim for the prior year.

See Form 8863 or the IRS Pub 970 for more information.

Box 7- If checked indicates that Box 1 includes amounts for an academic period beginning

in the next calendar year beginning January-March. See the IRS Pub. 970 for how to

report these amounts.

Box 8- Indicates whether you are considered to be carrying at last one-half the normal

full-time workload for your course of study at the University of Tennessee. If you

are at least a half-time student for at least one academic period that begins during

the year, you meet one of the requirements for the Hope credit. You do not have to

meet the workload requirement to qualify for the tuition and fees deduction or the

lifetime learning credit.

Box 9- Indicates whether you are considered to be enrolled in a program leading to a graduate

degree, graduate-level certificate, or other recognized graduate-level educational

credential. If you are enrolled in a graduate program, you are not eligible for the

Hope credit, but you may qualify for the tuition and fees deduction or the lifetime

learning credit.

Box 10-This box will always be blank on 1098-T form the student receives from the University

of Tennessee.

The University cannot provide tax advice. Please consult your tax professional to

find out more about your eligibility for tax credits and/or the taxability of your

scholarships.